Imagine you are the founder of a small bootstrapped company, and your business has just started to break even (you are finally out of the woods of operating at a loss). But suddenly, your tax bill arrives, and you owe a huge amount of money to the government. This is exactly what happened to many startup founders in 2023. The culprit? Section 174.

A simple section in a 2017 bill drastically changed the game for the startup sector in the US, causing engineering jobs to be lost through massive layoffs or frozen hirings (especially if it's done abroad) and drops in R&D spending. But a winner may come out on top: foreign software companies.

Throughout this blog post, we'll aim to explain everything about this not-much-talked regulation that is likely to change, at least in the short term, the startup ecosystem in the US: how this came to be, what it is, its consequences, and what it means to you.

Breaking Down Section 174

Where it all began

Research and development (R&D) costs have long been considered regular expenses. This helped lower the company's taxes because it reduced the profits that were taxed, encouraging spending in R&D.

However, it all gave a turn in 2017 with the “Tax Cuts and Jobs Act”. Said act had to be designed to not add to the government's long-term budget deficit. To achieve this, one strategy was including provisions that would increase tax revenue in the future, even though the people who created the law expected to cancel or change those provisions before they actually took effect. This approach was taken because the law needed to balance its financial impact over 10 years to avoid a filibuster*. Section 174 was one of these provisions.

This section changes R&D costs from regular expenses that could be subtracted immediately to expenses that could only be amortized over five years (15 if the R&D was done abroad). But even more surprising was that Congress couldn't reach an agreement, and what was supposed to be a temporary measure became permanent.

*filibuster: a political strategy where legislative members prolong a debate to stall or stop a decision on a proposed law.Implications in the software industry

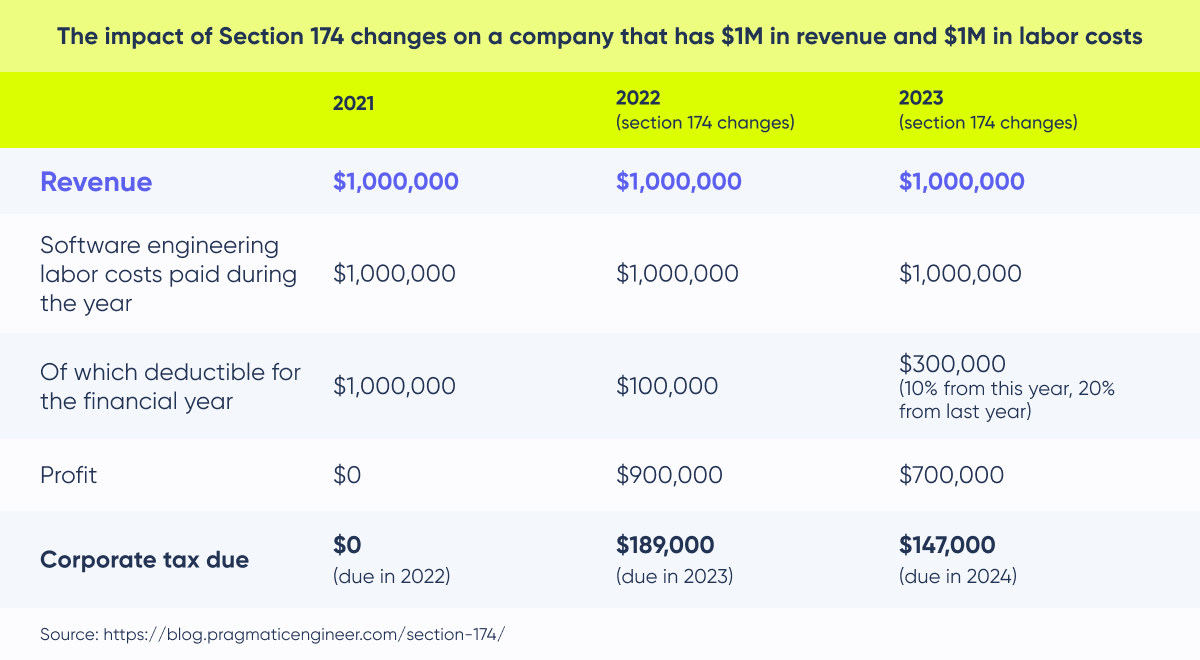

This section makes employing software engineers no longer considered a direct expense, and so it can't be deduced from the profits when they are paid their wages. Instead, expenses related to software development have to be amortized (depreciated) over five years, and 15 if the developer in question is working from abroad.

The most common example is the following: If a company has 1 million dollars in yearly revenue for a SaaS but employs five engineers to develop said service at a rate of 200.000 yearly salaries, the total profit would be zero (1.000.000 in revenue minus the 1.000.000 in labor cost). So they wouldn't have to pay taxes on that non-existing profit.

However, with Section 174 (which considers virtually all software development as R&D), the expenses (meaning the engineer's wages) linked to their SaaS and its 1 million revenue have to be differed throughout the next five years, making the profit for that company go from 0 to 900.000 (1.000.000 minus the 10% of expenses in the first year). So now, the company has a taxable profit of 900.000, a profit which is simply not there as they already pay the wages.

How it affects large companies

Big companies with large revenues beyond their R&D investments can endure these extra financial costs. However, they still have advocated changing this scenario through lobbyists, trade associations, or coalitions such as the R&D Coalition (created in 2018 and integrated by companies such as Amazon, Microsoft, and Intel).

This post by The Pragmatic Engineer has gathered the extent to which some large US businesses are being affected by Section 174:

For Google, the tax change was minimal because it was voluntarily amortizing software development expenses for most staff already.

How it affects small companies

Of course, the above situation only applies to smaller, bootstrapped businesses. According to a 2023 piece by Stratechery, many were completely blindsided by the situation or didn't measure its true consequences. They only found out through their accountant when the tax bill arrived, and they were being taxed on profits they weren't making.

This lack of awareness might be due to the little coverage Section 174 has received in mass media and the smaller companies' inability to lobby or affect policy-making or bill-passing, unlike large corporations. They have, however, tried to make themselves heard by forming coalitions such as the Small Software Business Alliance. According to its founder, Michele Hansen, little awareness of this massive change comes down to three main factors:

- There's a general belief that only large companies are affected by tax changes.

- People find tax policy issues dull and it only makes it to the headline when there's a significant social impact (say, widespread job layoffs).

- Section 174 was never meant to take effect, so concern about it was minimal.

Consequently, small companies now owe large sums of money to the government and were forced to make drastic financial decisions to make up for the drained cash flow. Some of them were forced to take out loans, extend credit lines (in this economy of increasing interest rates), or ask venture capitalists for more funding (in VC funding's worst year in a decade).

Many also had to resort to layoffs and hiring freezes. This does nothing to help a sector that's leading in job losses and has not seen a rate this high since the dot-com bubble burst in 2001. Startups might have to opt for slower development times with less staff.

Future Implications for the Startup Ecosystem

The U.S. startup environment relies on a careful equilibrium between venture capital funding, advanced engineering, and favorable tax conditions.

As is expected, these measures do nothing to help boost the startup ecosystem, creating a hostile environment for self-funded companies and startups that were already having a bad time as it was getting funding either from VCs or financial institutions operating at high rates.

All these factors contribute to the US becoming a hostile environment for startups and, what's more, slow down innovation and advancement through less investment in R&D, which is at the core of it all.

It could also mean less in-house development, as smaller companies will opt to outsource certain services and processes to avoid dealing with the financial burden of investing in research themselves. This is good news for specific companies that might benefit from an inflow of clients, but it also increases the sector's imbalance, making smaller companies dependent on larger ones.

There's a Possible Winner In All This

The US becoming less competitive in software development means other countries become more so. Now more than ever, starting tech companies outside the US is a more appealing move. Moreover, many US companies will find a legal loophole in all of this that makes opening a foreign subsidiary to carry out R&D a solution.

Another way out is to, instead of firing foreign developers carrying out R&D (because, as we mention, research and development being carried out abroad has to be amortized in 15 years), hire them as external vendors and charge that expense as “expense to suppliers" instead of R&D. This gives foreign developers an advantage over those located in the US.

However, it should be considered that the US is still a leading country in innovation and one of the main tech hubs. This means that a situation like this, in the long run, can't benefit global innovation as a whole.

The Light at The End of The Tunnel

As we mentioned, large and small companies tried to change this policy, and Congress appeared to listen to some extent. They are currently considering a new tax bill called the Tax Relief for American Families and Workers Act of 2024.

This bill aims to make some changes in the effects of Section 174, mainly bringing back the ability for companies to immediately deduct certain research and experimentation costs rather than spreading them out over time. This change would apply retroactively, meaning it would affect tax returns from 2023 to 2024, providing relief to startups that were facing negative tax consequences.

However, delaying the capitalization of these costs would be until 2026, when Section 174 would become effective again. It's also worth noting that R&D costs incurred outside the U.S. would still be spread out over the following 15 years, which is incredibly bad news for foreign engineers working remotely for the US.

Conclusion

There's no way of telling how this will end or the true consequences it will have, but it's somehow worrying that a bill with so many implications for the largest startup ecosystem in the world has gone unnoticed. And although we mentioned possible benefited parties, there are many that will be facing harsh and serious consequences.

Keep updated on the latest developments in the situation by following us on social media and subscribing to our updates!